Explore by category

What is the total annual loan cost (TALC) for reverse mortgages?

In this article:

- What is the total annual loan cost (TALC)?

- Why reverse mortgages use TALC disclosures

- TALC vs. APR: What’s the difference?

- What reverse mortgage costs are included in a TALC disclosure?

- How TALC is calculated

- How to read a TALC table

- Why TALC is usually higher over shorter loan terms

- How appreciation and non-recourse protections affect TALC

- Why 93% of home value appears in TALC disclosures

- How to use TALC when comparing reverse mortgages

- What disclosures do you receive with a reverse mortgage?

- Next steps: Using TALC to evaluate your options

- FAQs

Quick Answer: The total annual loan cost (TALC) is a reverse mortgage disclosure that estimates how borrowing costs may change over time. TALC projections help borrowers understand how factors such as loan duration, home appreciation, interest rates, fees, and the growing loan balance that may result from negative amortization affect the long-term cost of a reverse mortgage.

Key Points

Reverse mortgage TALC projections are often higher over shorter time periods because upfront costs are spread across a smaller window.

Unlike annual percentage rate (APR), TALC calculations take into consideration factors such as home appreciation, loan duration, and deferred repayment timelines.

Reviewing TALC disclosures carefully may help borrowers better understand how long-term borrowing costs could affect their home equity over time.

Reverse mortgage paperwork may include a long list of unfamiliar terms and disclosures—and one of the most important is the total annual loan cost, or TALC. While the term may sound technical, the TALC disclosure is intended to give borrowers a clearer picture of how reverse mortgage costs may change over time.

Because reverse mortgages work differently than traditional mortgages, borrowing costs may vary considerably depending on factors such as loan duration, home appreciation, interest rates, and payout structure. Reviewing the TALC disclosure carefully may help you better understand how a reverse mortgage could affect your long-term borrowing costs and home equity.

What is the total annual loan cost (TALC)?

The TALC is a disclosure included in your reverse mortgage paperwork to help you estimate how borrowing costs may change over time. Unlike annual percentage rate (APR), TALC projections account for factors such as interest, fees, mortgage insurance premiums, home appreciation, and loan duration.

For Home Equity Conversion Mortgages (HECMs), lenders are required by the U.S. Department of Housing and Urban Development (HUD) to provide a TALC disclosure as part of the application process. Under Consumer Financial Protection Bureau (CFPB) rules, the TALC rate is an annualized estimate used to illustrate how projected borrowing costs may change under different scenarios.

It’s important to note TALC is an estimate—not a guarantee. Actual reverse mortgage costs may vary substantially depending on future interest rates, home values, and how long you have the loan.

Why reverse mortgages use TALC disclosures

Reverse mortgage lenders provide TALC disclosures to help borrowers understand how the cost of a reverse mortgage may change over time. Unlike traditional mortgages with fixed repayment schedules, reverse mortgage repayment is generally deferred until the borrower sells the home, moves out permanently, passes away, or fails to meet the loan terms. As a result, loan duration and total borrowing costs may differ widely from one borrower to another.

TALC disclosures also take the unique cost structure of reverse mortgages into consideration, including accruing interest, mortgage insurance premiums, servicing fees where applicable, and financed closing costs that may be added to the loan balance over time. By showing how borrowing costs may change under different circumstances, TALC disclosures may help borrowers make more informed decisions and better understand how a reverse mortgage may affect them over time.

To learn more, please visit the CFPB’s “Reverse Mortgage: A Discussion Guide.”

The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, and hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

TALC vs. APR: What’s the difference?

TALC and APR are designed to help borrowers understand loan costs, but they serve different purposes.

APR is commonly used for loans with predictable repayment schedules, specified loan terms, and fixed amortization timelines, which show how the loan balance decreases according to a predetermined repayment schedule. APR combines interest rates and certain fees into a single percentage intended to help borrowers compare total borrowing costs.

Reverse mortgages work differently. Because repayment is generally deferred and the loan balance may increase over time through a process known as negative amortization, costs depend on factors such as loan duration, home appreciation, interest rates, and payout structure. Many factors that may affect the long-term cost of a reverse mortgage—such as home appreciation and repayment timing—are not reflected in a single APR figure.

| Feature | TALC | APR |

| Primarily used for | Reverse mortgages | Traditional mortgages and other consumer loans |

| Accounts for loan duration | Yes | Limited |

| Accounts for home appreciation scenarios | Yes | No |

| Reflects multiple future scenarios | Yes | No |

| Uses a single standardized rate | No | Yes |

| Purpose | Evaluating potential long-term reverse mortgage costs | Evaluating loans with predictable repayment schedules |

Why this matters: APR provides a single cost figure based on a defined loan structure, while TALC illustrates how reverse mortgage costs may vary under different timelines and home appreciation scenarios.

What reverse mortgage costs are included in a TALC disclosure?

TALC disclosures account for several costs associated with a reverse mortgage. The expenses reflected in TALC projections may include:

- Interest charges: Because reverse mortgages generally do not require monthly principal and interest payments, interest accrues and the outstanding loan balance grows over time.

- Mortgage insurance premiums: For HECMs, insurance from the Federal Housing Administration (FHA) helps provide borrower safeguards, including non-recourse protections that limit repayment obligations to the home’s value under qualifying circumstances.¹

- Origination fees: These initial loan charges help cover the cost of processing the reverse mortgage and are often financed into the loan rather than paid out of pocket upfront, which means interest may accrue on those amounts over time.

- Servicing fees: Some lenders may charge ongoing monthly loan charges associated with administering the loan.

- Closing costs: These may include expenses such as appraisals, title services, and recording fees.

While reverse mortgages generally do not require monthly principal and interest payments, borrowers must continue to meet loan obligations, including paying property taxes, maintaining homeowners insurance, and keeping the home in good condition. If those obligations are not met, the reverse mortgage may become due and payable.

→ Learn more: Reverse mortgage fees and costs explained

The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, and hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

How TALC is calculated

A TALC disclosure shows how the cost of a reverse mortgage may change under different assumptions and expresses those projected costs as an annualized rate. These calculations follow standardized disclosure requirements established under the Truth in Lending Act (TILA), a federal law designed to promote transparency and help consumers compare borrowing costs. Because reverse mortgages do not have fixed repayment timelines, TALC calculations rely on multiple factors.

Key factors that may affect TALC projections include:

- Age of the youngest borrower: Borrower age affects both the available loan amount and expected loan duration. Younger borrowers may have different projected costs because the repayment timeline may be longer.

- Home value: Reverse mortgage borrowing limits are partially based on the appraised value of the property. Higher-value homes may allow borrowers to access more home equity.

- Interest rates: Changes in borrowing rates may affect how quickly the loan balance grows over time. TALC calculations may also be influenced by the loan’s initial interest rate.

- Payment option: Borrowers may choose a lump sum advance, monthly advance payments, a credit line arrangement, or combination payout structure. Each option may affect how quickly loan proceeds are accessed and how costs accumulate over time.

→ Read more: Understanding reverse mortgage payout options

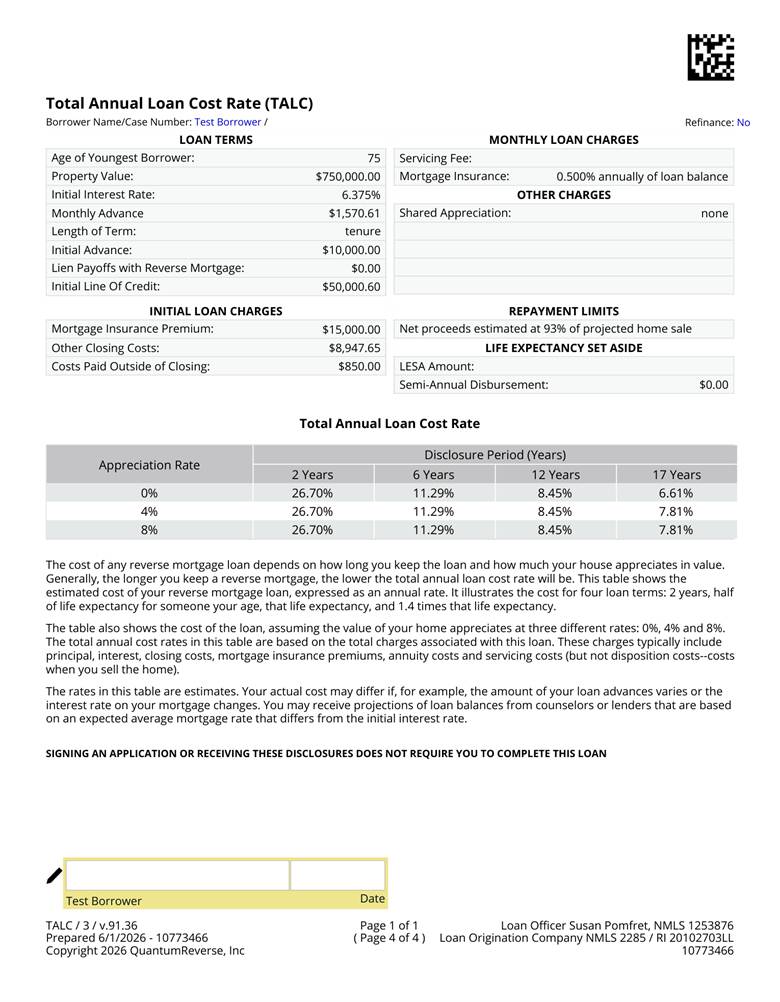

How to read a TALC table

A TALC disclosure typically includes a table showing the estimated cost of a reverse mortgage across different timelines and home appreciation assumptions. For federally insured HECMs, TALC disclosures are typically presented using a standardized model form or sample form required by federal guidelines.

TALC projections are usually presented across multiple disclosure periods, such as two years, five years, the borrower’s life expectancy, and other extended timeframes. Because reverse mortgage costs are heavily influenced by loan duration, projected annual costs may differ significantly across these timelines.

Under federal disclosure requirements, TALC tables for HECMs commonly include projected home appreciation rates of 0%, 4%, and 8%. The table then estimates average annual loan costs for each scenario based on factors such as interest, mortgage insurance premiums, fees, and financed costs.

In many cases, reverse mortgages become less expensive on an annualized basis the longer the borrower remains in the home because upfront costs are spread across more time. As a result, TALC rates often decrease as loan duration increases.

The simplified example below illustrates how projected TALC figures may change depending on loan duration.

| Loan duration | Assumed home appreciation | Projected TALC |

| 2 years | 4% | Higher projected annual cost |

| 5 years | 4% | Moderate projected annual cost |

| 10 years | 4% | Lower projected annual cost |

| Life expectancy | 4% | Lower projected annual cost |

An actual TALC disclosure contains additional details, including loan terms, fees, repayment assumptions, and multiple home appreciation scenarios. The sample disclosure below shows how TALC projections may be presented in practice.

Notice that the disclosure includes multiple projected appreciation rates and disclosure periods. The resulting TALC figures represent annualized cost estimates, expressed as an annual rate under different scenarios.

In addition to projected cost estimates, TALC disclosures include standardized information required under federal disclosure rules. For example, TALC forms state that receiving the disclosure does not obligate a borrower to complete the reverse mortgage loan.

An important caveat: TALC is not a prediction of the total cost of a reverse mortgage. Instead, it is an estimated cost based on assumptions about future home values, interest accrual, and how long the borrower remains in the home.

For many homeowners, the most important takeaway is that TALC is designed to help compare possible outcomes—not predict exactly what a reverse mortgage will cost in the future.

Why TALC is usually higher over shorter loan terms

To help put this into perspective, imagine a homeowner named Josephine reviewing a TALC disclosure for a reverse mortgage. The table shows projected annual loan costs over several timeframes, including three years and 20 years.

At the three-year mark, the projected TALC may appear relatively high because upfront costs such as origination fees, mortgage insurance premiums, and closing costs are spread across a shorter period. At the 20-year mark, the projected TALC may appear lower on an annualized basis because those same upfront costs are distributed across a longer timeframe.

Because TALC is expressed as an annualized rate, a lower TALC figure does not necessarily mean the reverse mortgage will cost less overall. Over longer periods, the loan balance and total borrowing costs may continue to increase as interest and other charges accrue, even as the annualized TALC rate declines.

How appreciation and non-recourse protections affect TALC

Home appreciation assumptions play an important role in TALC calculations because future changes in property values may affect how much equity remains relative to the reverse mortgage balance over time.

In general, stronger home appreciation may reduce projected TALC figures because the property is assumed to gain value more quickly relative to the loan balance. Slower appreciation may result in higher projected costs because the reverse mortgage balance may consume a larger share of available equity.

For HECMs, non-recourse protections also affect TALC projections. FHA insurance helps support the non-recourse feature, which generally prevents borrowers or their heirs from owing more than the home’s value when the loan becomes due.1 The cost of that insurance is reflected in TALC calculations through FHA mortgage insurance premiums.

Why 93% of home value appears in TALC disclosures

When reviewing reverse mortgage paperwork, you may notice that TALC disclosures often reference a figure equal to 93% of the home’s projected value. While the number may seem confusing at first, it is part of the standardized approach used in HECM cost projections.

Under HUD’s TALC disclosure requirements for HECMs, certain projections are based on 93% of the home’s projected future value when illustrating estimated borrowing costs. The figure is part of a standardized disclosure formula and should not be interpreted as a guarantee of future equity or sale proceeds.

How to use TALC when comparing reverse mortgages

TALC disclosures may help borrowers compare reverse mortgage options by showing how costs could change under different circumstances. Reviewing TALC tables side by side may help borrowers evaluate differences in lender fees, interest rates, payout structures, and long-term borrowing costs.

TALC projections may also help borrowers compare different payout options, such as lump sums, monthly advance payments, and lines of credit. Because reverse mortgage costs are heavily influenced by loan duration, TALC disclosures may be especially useful for homeowners considering how long they expect to remain in their homes.

By reviewing different appreciation scenarios and projected loan timelines, borrowers may gain a clearer understanding of how a reverse mortgage could affect home equity and long-term retirement planning.

What disclosures do you receive with a reverse mortgage?

In addition to the TALC, reverse mortgage borrowers receive several other disclosures and estimates explaining loan terms, projected costs, and borrower obligations.

One of the most important is the amortization schedule, which illustrates how the reverse mortgage balance may change over time as interest, mortgage insurance premiums, and financed costs accumulate. Unlike a traditional mortgage amortization schedule, which typically shows a declining loan balance over time, a reverse mortgage amortization schedule often reflects a growing balance as interest and other costs are added to the loan through a process known as negative amortization.

Borrowers also receive closing disclosures summarizing the final loan terms and costs, including interest rates, fees, payout structures, and financed expenses. Earlier in the process, loan estimates provide an initial overview of projected costs and loan terms.

For HECMs, borrowers must also complete a session with a HUD-approved counselor before the loan can move forward. Afterward, borrowers receive a certificate confirming completion of the requirement.

Next steps: Using TALC to evaluate your options

The TALC disclosure is one tool that may help borrowers compare reverse mortgage options and better understand how factors such as timing, interest rates, and home appreciation could affect long-term borrowing costs.

Because every borrower’s situation is different, it may be helpful to review TALC projections alongside other reverse mortgage estimates, repayment considerations, and retirement planning goals.

For homeowners considering whether a reverse mortgage may fit into their retirement strategy, Finance of America’s reverse mortgage calculator may provide a helpful starting point for estimating available home equity based on factors such as age, home value, and location.

FAQs

Is TALC the same as APR?

No. TALC and APR are different disclosures. APR is commonly used for traditional loans with fixed repayment schedules, while TALC was designed specifically for reverse mortgages because repayment timing and borrowing costs may vary significantly.

Does the TALC disclosure include reverse mortgage fees?

Yes. TALC projections generally include many costs associated with the reverse mortgage, including interest charges, mortgage insurance premiums, origination fees, servicing fees where applicable, and financed closing costs.

Can tax considerations affect the cost of a reverse mortgage?

Potentially. In some circumstances, interest paid on a reverse mortgage may be tax-deductible when the loan is repaid, which could affect the overall cost of borrowing. However, tax treatment depends on individual circumstances and applicable tax laws. TALC disclosures do not account for potential tax deductions, so borrowers should consult a qualified tax professional for guidance.

Can my actual costs differ from what the TALC table shows?

Yes. TALC disclosures are estimates, not guarantees. The actual cost may differ from the estimated cost shown in the TALC table depending on factors such as interest rates, home appreciation, loan duration, and the timing and amount of loan advances received over time.

What do lenders use to calculate TALC?

TALC calculations are based on several factors, including borrower age, home value, interest rates, loan costs, projected home appreciation, and the payment option selected. Because reverse mortgages do not have fixed repayment timelines, these variables help lenders estimate how borrowing costs may change under different scenarios.

Is TALC used for proprietary (non-HECM) reverse mortgages?

TALC disclosures are most closely associated with HECMs, which are federally insured reverse mortgages subject to HUD disclosure requirements. Proprietary reverse mortgage products may use different disclosure structures depending on the loan type, lender requirements, and applicable regulations.

How early in the process will I receive a TALC disclosure?

Borrowers generally receive TALC disclosures during the early stages of the reverse mortgage application process as part of required loan documentation.

1Non-recourse means that you, or your estate, can’t owe more than the value of your home when the loan becomes due and the home is sold.

Non-recourse means that if you default on the loan, or if the loan cannot otherwise be repaid, the lender cannot look to your other assets (or your estate’s assets) to meet the outstanding balance on your loan.

About the author

is a Senior Web Content Writer at Finance of America and a journalist with more than 20 years of experience specializing in business, and technology. Her work has been published in The Wall Street Journal, The Financial Times, and numerous other leading outlets.

Disclaimer

This article is intended for general informational and educational purposes only and should not be construed as financial or tax advice. For tax advice, please consult a tax professional. For more information about whether a reverse mortgage fits into your retirement strategy, you should consult your financial advisor.